In today’s complex regulatory environment, SOC 1 compliance has become a critical business requirement for service organizations handling financial data. This comprehensive guide provides everything security and compliance professionals need to navigate the SOC 1 certification process successfully, from initial preparation through ongoing compliance maintenance.

Understanding SOC 1 Compliance

What Is SOC 1 Compliance?

SOC 1 (System and Organization Controls 1) is an auditing standard developed by the American Institute of Certified Public Accountants (AICPA) specifically for service organizations that impact their clients’ financial reporting. Unlike broader security frameworks, SOC 1 focuses exclusively on controls relevant to financial statements and reporting integrity.

The standard provides a structured framework for evaluating and reporting on the design and operational effectiveness of internal controls that could affect the accuracy and reliability of clients’ financial statements. SOC 1 reports come in two types:

- Type I: Evaluates the design appropriateness of controls at a specific point in time

- Type II: Assesses both design appropriateness and operating effectiveness over a period (typically 6-12 months)

What Are the SOC 1 Requirements?

SOC 1 compliance requires organizations to implement and maintain controls across five foundational categories:

- Control Environment: The foundation of an effective internal control system, encompassing organizational structure, management philosophy, integrity, ethical values, and commitment to competence.

- Risk Assessment: Systematic processes for identifying and analyzing risks related to financial reporting objectives, including both internal and external factors.

- Control Activities: Specific policies and procedures implemented to address identified risks and ensure management directives are carried out effectively.

- Information and Communication: Systems for capturing, processing, and exchanging information needed for financial reporting, including both automated and manual processes.

- Monitoring Activities: Ongoing and periodic assessments to evaluate control effectiveness and address deficiencies promptly.

Within each category, organizations must implement specific controls tailored to their unique services, systems, and risk profile. These controls must be formally documented, regularly tested, and continuously monitored.

What Are the Benefits of SOC 1?

Achieving SOC 1 compliance delivers substantial benefits beyond mere regulatory checkbox exercises:

- Enhanced Client Trust: Demonstrates commitment to maintaining robust financial controls

- Competitive Advantage: Increasingly required in RFPs and vendor selection processes

- Improved Internal Controls: Identifies and addresses control weaknesses before they impact operations

- Reduced Audit Fatigue: Consolidates multiple client audit requests into a single comprehensive report

- Risk Reduction: Systematically identifies and mitigates financial reporting risks

- Operational Efficiency: Streamlines processes through standardized control implementation

Organizations that approach SOC 1 strategically often discover operational improvements that extend far beyond compliance requirements, creating lasting value through enhanced process discipline and control effectiveness.

Who Needs a SOC 1 Audit?

SOC 1 audits are specifically designed for service organizations whose services impact their clients’ financial statements. Organizations typically requiring SOC 1 certification include:

- Payment processors and financial technology companies

- Payroll service providers

- Loan servicing organizations

- Claims processing services

- Trust services

- Managed IT service providers supporting financial systems

- Data center operators hosting financial applications

- Software-as-a-Service (SaaS) providers offering financial applications

The need for SOC 1 compliance is determined by whether your services could materially impact your clients’ financial reporting processes or financial statement accuracy. If clients rely on your controls as part of their own financial reporting processes, SOC 1 certification is likely necessary.

SOC 1 vs. SOC 2: What’s the Difference?

While both SOC 1 and SOC 2 evaluate organizational controls, they serve fundamentally different purposes and address distinct requirements:

SOC 1

- Focus: Internal controls over financial reporting

- Audience: Primarily clients’ financial management, auditors, and regulators

- Framework: Based on SSAE 18 (Statement on Standards for Attestation Engagements)

- Control Criteria: Custom controls defined by the service organization based on financial reporting impact

- Report Distribution: Restricted to management, existing clients, and their auditors

SOC 2

- Focus: Controls related to security, availability, processing integrity, confidentiality, and privacy

- Audience: Broader stakeholders concerned with security and operational excellence

- Framework: Based on the AICPA’s Trust Services Criteria

- Control Criteria: Standardized criteria across five trust service categories

- Report Distribution: Still restricted but typically shared with prospective clients under NDA

Many organizations require both SOC 1 and SOC 2 compliance, as they address complementary but distinct control objectives. While SOC 1 focuses narrowly on financial reporting controls, SOC 2 addresses broader security and operational concerns.

SOC 1 Compliance Checklist

Achieving SOC 1 compliance requires a systematic approach encompassing 22 essential steps across planning, implementation, testing, reporting, and maintenance phases:

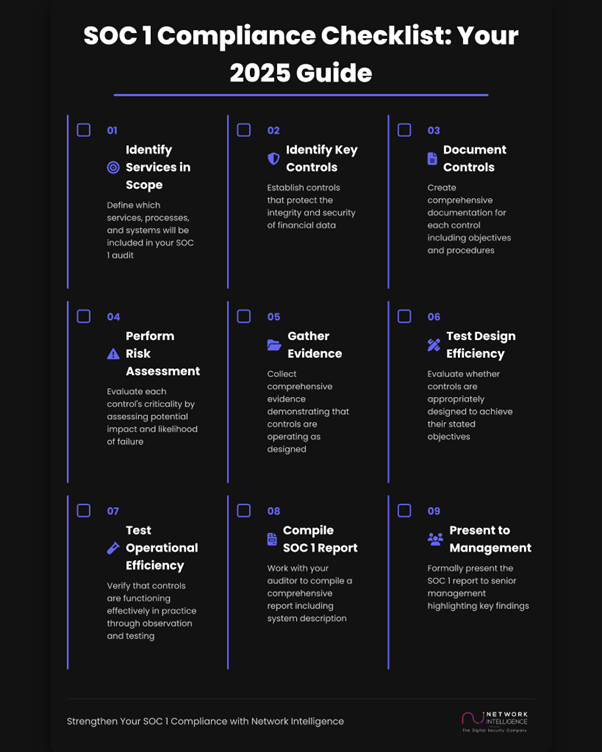

Identify the Services Within the Scope of the SOC 1 Audit

Begin by clearly defining which services, processes, and systems will be included in your SOC 1 audit. This critical scoping exercise should:

- Identify all services that could impact clients’ financial reporting

- Document system boundaries and interconnections

- Map data flows relevant to financial processing

- Determine which locations and facilities are in scope

- Identify relevant subservice organizations

Proper scoping prevents scope creep during the audit process and ensures resources are focused on truly relevant controls. Work closely with your auditor during this phase to ensure alignment on scope boundaries.

Identify Key Financial Controls

Once scope is established, identify specific controls that protect the integrity, accuracy, and security of financial data and processes. Key financial controls typically include:

- Access controls: Ensuring only authorized personnel can access financial systems and data

- Change management: Controlling modifications to financial applications and infrastructure

- Data validation: Verifying the accuracy and completeness of financial data

- Processing controls: Ensuring transactions are processed accurately and completely

- Reconciliation procedures: Confirming data consistency across systems

- Segregation of duties: Preventing conflicts of interest in financial processes

- Backup and recovery: Protecting against data loss

Each identified control should have a clear owner, documented procedures, and defined testing methodologies.

Control Objectives & Design

For each identified control, establish clear objectives that articulate what the control is intended to accomplish. Well-designed control objectives should be:

- Specific and measurable

- Aligned with financial reporting requirements

- Focused on risk mitigation

- Realistic and achievable

- Time-bound where appropriate

Control design should incorporate the principle of defense in depth, with multiple complementary controls addressing critical risks rather than relying on single control points.

Document the Description of Controls

Create comprehensive documentation for each control, including:

- Detailed control descriptions

- Control objectives and intended outcomes

- Control owners and responsible parties

- Control frequency (continuous, daily, weekly, monthly, etc.)

- Implementation methods (automated, manual, or hybrid)

- Evidence generated during control operation

- Testing procedures and expected results

This documentation forms the foundation of your SOC 1 report and provides essential guidance for both control operators and auditors.

Perform a Risk Assessment on Each Identified Control

Evaluate each control’s criticality by assessing:

- Potential impact if the control fails

- Likelihood of control failure

- Complexity of the control implementation

- Dependencies on other controls or systems

- Historical performance and reliability

- Regulatory requirements related to the control

This risk assessment helps prioritize testing efforts and identify controls requiring enhanced monitoring or redundancy.

Plan the SOC 1 Audit

Develop a comprehensive audit plan including:

- Audit timeline and key milestones

- Resource requirements and assignments

- Testing methodologies for each control

- Evidence collection procedures

- Reporting templates and formats

- Communication protocols with the audit team

- Escalation procedures for identified issues

A well-structured audit plan ensures efficient use of resources and minimizes disruption to normal operations during the audit process.

Conduct a Readiness Assessment

Before the formal audit begins, perform a thorough readiness assessment to:

- Identify potential control gaps or weaknesses

- Test control documentation for completeness

- Verify evidence availability and quality

- Assess staff preparedness for the audit

- Identify and address potential issues proactively

This pre-audit assessment significantly increases the likelihood of a successful formal audit and reduces the risk of unexpected findings.

Gather Evidence Supporting the Operating Effectiveness of Each Control

Collect comprehensive evidence demonstrating that controls are operating as designed. Effective evidence typically includes:

- System-generated reports and logs

- Screenshots of configuration settings

- Approval documentation

- Change management records

- Access review documentation

- Exception handling records

- Training completion records

Evidence should be organized systematically and mapped directly to specific controls to facilitate efficient auditor review.

Test the Design Efficiency of Each Control

Evaluate whether controls are appropriately designed to achieve their stated objectives by:

- Reviewing control documentation against best practices

- Assessing whether controls address identified risks

- Evaluating control precision and specificity

- Identifying potential control gaps or overlaps

- Verifying alignment with regulatory requirements

Design efficiency testing focuses on whether controls would be effective if operating as designed, regardless of actual implementation.

Test the Operational Efficiency of Each Control

Verify that controls are functioning effectively in practice through:

- Observation of control execution

- Examination of control evidence

- Re-performance of control activities

- Inquiry with control operators

- Sample testing across the audit period

- Exception analysis and root cause assessment

Operational testing confirms that well-designed controls are actually delivering their intended protection in real-world operations.

Review and Document the Results of Testing

Thoroughly document all testing activities and results, including:

- Testing methodologies used

- Samples selected and testing criteria

- Test results for each control

- Identified exceptions or deviations

- Root cause analysis for any failures

- Remediation plans for identified issues

- Evidence supporting test conclusions

This documentation provides the foundation for auditor evaluation and supports continuous improvement efforts.

Evaluate Any Identified Exceptions or Deficiencies

For any control failures or exceptions, conduct thorough analysis to:

- Determine the root cause of the failure

- Assess the potential impact on financial reporting

- Evaluate whether compensating controls mitigate the risk

- Develop appropriate remediation plans

- Implement immediate corrective actions where necessary

- Establish monitoring to prevent recurrence

Proper exception handling demonstrates control maturity and commitment to continuous improvement.

Compile the SOC 1 Report

Work with your auditor to compile a comprehensive SOC 1 report including:

- Management assertion regarding control effectiveness

- Service auditor’s opinion

- System description and scope

- Control objectives and related controls

- Test procedures and results

- Identified exceptions and management responses

- Complementary user entity controls

The report should provide a clear, accurate representation of your control environment and testing results.

Approval: Audit Lead on Final SOC 1 Report

Ensure formal review and approval of the draft report by the audit lead, focusing on:

- Accuracy and completeness of the report

- Appropriate characterization of exceptions

- Clarity of management responses

- Alignment with audit evidence

- Compliance with AICPA reporting standards

This review ensures the report meets professional standards before presentation to management.

Present the SOC 1 Report to Management

Formally present the SOC 1 report to senior management, highlighting:

- Overall audit results and opinion

- Significant findings and their implications

- Required remediation activities

- Recommendations for control improvements

- Timeline for addressing identified issues

- Resources required for remediation

Management presentation ensures organizational awareness of audit results and secures commitment for necessary improvements.

Discuss Corrective Actions for Identified Deficiencies

Develop detailed corrective action plans for any identified deficiencies, including:

- Specific remediation activities

- Responsible parties for each action

- Implementation timelines

- Required resources

- Success criteria and verification methods

- Monitoring procedures to prevent recurrence

Well-structured remediation plans demonstrate commitment to addressing identified issues promptly and effectively.

Monitor Corrective Actions Implementation

Establish a formal process to track remediation progress, including:

- Regular status updates from action owners

- Evidence collection demonstrating implementation

- Validation testing of implemented changes

- Escalation procedures for delayed remediation

- Management reporting on remediation status

- Documentation of completed actions

Effective monitoring ensures timely completion of corrective actions and provides evidence for future audits.

Retest Failed Controls

Once remediation is complete, conduct formal retesting to:

- Verify that remediated controls now function effectively

- Ensure no unintended consequences from changes

- Document the effectiveness of remediation

- Provide evidence for updating the audit report

- Confirm that identified risks are now properly mitigated

Retesting provides assurance that control deficiencies have been properly addressed.

Approval: Management on Corrective Actions

Secure formal management approval of completed remediation activities, confirming:

- Satisfaction with implemented changes

- Acceptance of any residual risks

- Commitment to maintaining improved controls

- Understanding of ongoing monitoring requirements

- Approval of updated control documentation

Management approval demonstrates organizational commitment to the remediated control environment.

Revise the SOC 1 Report Based on Retesting and Management’s Response

Update the SOC 1 report to reflect:

- Results of control retesting

- Management’s response to identified issues

- Implemented remediation activities

- Status of outstanding remediation

- Updated control descriptions where applicable

The revised report should accurately reflect the current state of controls, including improvements made during the audit process.

Issue the Final SOC 1 Report

Distribute the final approved report to authorized recipients, including:

- Internal stakeholders (management, board, etc.)

- Existing clients as contractually required

- Client auditors upon appropriate request

- Regulatory bodies where mandated

Maintain strict distribution control in accordance with AICPA requirements, as SOC 1 reports contain sensitive information about control environments.

Maintain All Documentation for at Least Five Years

Establish a secure repository for all audit-related documentation, including:

- Control descriptions and objectives

- Test plans and results

- Evidence collected during testing

- Exception documentation and root cause analysis

- Remediation plans and implementation evidence

- Final and draft reports

- Auditor correspondence

AICPA standards require retention of this documentation for a minimum of five years to support future audits and potential regulatory inquiries.

Preparing for a SOC 1 Audit

How Long Does a SOC 1 Audit Take to Complete?

The SOC 1 audit timeline varies based on organizational complexity, control maturity, and audit scope, but typically follows this schedule:

- Planning and Scoping: 2-4 weeks

- Readiness Assessment: 2-6 weeks

- Control Documentation and Remediation: 4-12 weeks

- Type I Audit Execution: 2-4 weeks

- Type II Observation Period: 6-12 months

- Type II Testing and Reporting: 4-6 weeks

Organizations pursuing their first SOC 1 audit should plan for a 6-9 month process for Type I and 12-18 months for Type II certification. Subsequent audits typically require less preparation time as control documentation and processes mature.

How Much Does a SOC 1 Audit Cost?

SOC 1 audit costs vary significantly based on:

- Organization size and complexity

- Number of in-scope systems and processes

- Geographic distribution of operations

- Control maturity and documentation quality

- Audit type (Type I vs. Type II)

- Remediation requirements

Typical cost ranges include:

- Small organizations (Type I): $20,000-$40,000

- Medium organizations (Type I): $40,000-$75,000

- Large organizations (Type I): $75,000-$150,000+

Type II audits typically cost 25-50% more than Type I due to the extended testing period and increased evidence evaluation. Organizations should also budget for internal resource costs, potential remediation expenses, and ongoing compliance maintenance.

Internal Testing & Documentation

Effective internal testing prior to formal audit significantly increases success probability while reducing audit costs. Implement a structured testing program including:

- Control Self-Assessments: Regular operator evaluation of control effectiveness

- Internal Audit Reviews: Independent testing by internal audit teams

- Mock Audits: Simulated external audits to identify potential issues

- Continuous Monitoring: Automated tools to verify ongoing control operation

- Exception Tracking: Systematic logging and analysis of control failures

Comprehensive documentation should include detailed narratives, flowcharts, risk assessments, and evidence samples that demonstrate control effectiveness throughout the audit period.

Working with an Independent Auditor

Select an independent auditor with:

- Relevant industry experience

- SOC audit specialization

- Appropriate certifications (CPA, CISA, etc.)

- Reputation for thoroughness and professionalism

- Clear communication style

- Reasonable fee structure

Establish expectations early regarding communication protocols, evidence requirements, testing methodologies, and reporting timelines. Maintain professional skepticism while fostering collaborative problem-solving when issues arise.

Using a SOC 1 Audit Checklist

A well-structured SOC 1 audit checklist serves as a roadmap throughout the compliance process. Effective checklists should:

- Map directly to the 22 essential steps outlined earlier

- Include detailed sub-tasks for each major step

- Assign clear ownership for each activity

- Establish realistic timelines and dependencies

- Track completion status and outstanding items

- Identify potential bottlenecks and critical paths

- Incorporate lessons learned from previous audits

Regularly review and update the checklist as the audit progresses to ensure continued alignment with project realities and emerging requirements.

Common Challenges in SOC 1 Audits

Incomplete Documentation

Insufficient or unclear control documentation represents the most common audit challenge. Address this proactively by:

- Implementing standardized documentation templates

- Establishing clear documentation ownership

- Conducting regular documentation reviews

- Maintaining version control for all documents

- Creating clear linkages between controls and evidence

- Developing process narratives and flowcharts

Comprehensive documentation not only facilitates successful audits but also supports knowledge transfer and operational consistency.

Insufficient Control Testing

Inadequate control testing often results in unexpected audit findings. Strengthen testing practices by:

- Developing detailed test plans for each control

- Implementing risk-based sample selection

- Documenting test procedures and expected results

- Maintaining evidence of test execution

- Analyzing test failures and implementing corrections

- Conducting independent review of test results

Robust internal testing identifies and addresses control weaknesses before they become audit findings.

Managing Multiple Locations

Organizations with distributed operations face unique challenges in maintaining consistent controls across locations. Address these challenges by:

- Establishing standardized control frameworks

- Implementing centralized documentation repositories

- Conducting cross-location control assessments

- Leveraging technology for remote evidence collection

- Establishing clear local control ownership

- Developing location-specific implementation guidance

A balanced approach combining centralized governance with local implementation flexibility typically yields the best results.

Staff Awareness

Limited staff understanding of SOC 1 requirements and their specific control responsibilities can undermine compliance efforts. Enhance awareness through:

- Role-specific training programs

- Clear communication of control objectives

- Regular reinforcement of compliance importance

- Recognition of exemplary compliance practices

- Inclusion of compliance responsibilities in performance evaluations

- Accessible guidance for control execution

When staff understand both what they need to do and why it matters, control effectiveness significantly improves.

Key SOC 1 Audit Requirements for 2025

As financial systems evolve and threat landscapes change, SOC 1 requirements continue to adapt. Key focus areas for 2025 include:

Strong Security Controls

Modern SOC 1 audits increasingly emphasize robust security controls protecting financial data and systems, including:

- Identity and Access Management: Sophisticated authentication, authorization, and access review processes

- Encryption: Comprehensive data protection both at rest and in transit

- Vulnerability Management: Systematic identification and remediation of security weaknesses

- Patch Management: Timely application of security updates to all financial systems

- Security Monitoring: Continuous surveillance for potential security incidents

These controls must be formally documented, regularly tested, and continuously monitored to demonstrate effectiveness throughout the audit period.

Availability and Performance

System availability directly impacts financial reporting reliability. Key availability controls include:

- Redundancy: Elimination of single points of failure in critical systems

- Disaster Recovery: Comprehensive plans for recovering from service disruptions

- Capacity Management: Proactive monitoring and scaling to meet demand

- Performance Monitoring: Continuous tracking of system responsiveness

- Incident Management: Structured processes for addressing availability issues

Availability controls must be regularly tested through simulated failures and recovery exercises to verify effectiveness.

Processing Integrity

Controls ensuring accurate, complete, and timely transaction processing form the core of SOC 1 compliance. Critical processing integrity controls include:

- Input Validation: Verification of data accuracy and completeness before processing

- Processing Verification: Confirmation that transactions are processed correctly

- Error Handling: Systematic identification and resolution of processing exceptions

- Reconciliation: Regular comparison of data across systems to identify discrepancies

- Output Review: Verification of reporting accuracy and completeness

These controls must operate consistently throughout the audit period with appropriate evidence of their effectiveness.

Confidentiality and Privacy

Protection of sensitive financial information requires comprehensive confidentiality and privacy controls:

- Data Classification: Identification and appropriate handling of sensitive information

- Access Restrictions: Limiting data access based on legitimate business need

- Data Minimization: Collecting and retaining only necessary information

- Secure Disposal: Proper destruction of information when no longer needed

- Privacy Compliance: Adherence to relevant privacy regulations

These controls must address both technical and procedural aspects of information protection throughout the data lifecycle.

Continuous Monitoring and Incident Management

Modern SOC 1 requirements emphasize ongoing control verification rather than point-in-time assessments:

- Automated Monitoring: Continuous verification of control operation

- Exception Alerting: Immediate notification of control failures

- Incident Response: Structured processes for addressing control breakdowns

- Root Cause Analysis: Systematic investigation of control failures

- Continuous Improvement: Ongoing refinement of control design and implementation

Effective monitoring demonstrates control reliability throughout the audit period and supports rapid identification and remediation of issues.

What Information is Included in a SOC 1 Report?

A comprehensive SOC 1 report contains several key sections providing stakeholders with a complete understanding of your control environment:

Report Scope

Clearly defines which services, systems, and locations are included in the report, establishing boundaries for auditor evaluation and user reliance. The scope section should:

- Identify specific services covered

- Define system boundaries

- List included locations

- Specify the types of data and transactions addressed

- Identify any excluded components or services

Clear scope definition prevents misunderstanding about what the report does and does not cover.

Report Period

Specifies the timeframe covered by the report, which differs between report types:

- Type I: Reports on controls at a specific point in time

- Type II: Covers controls over a period, typically 6-12 months

The report period establishes when controls were evaluated and the duration of operating effectiveness testing for Type II reports.

Service Auditor

Identifies the independent CPA firm that conducted the audit, including:

- Firm name and location

- Lead auditor credentials

- Statement of independence

- Auditing standards followed

This information establishes the credibility and authority of the audit findings.

Auditor Opinion

Presents the auditor’s formal conclusion regarding:

- Fairness of management’s system description

- Suitability of control design

- Operating effectiveness of controls (Type II only)

The opinion may be unqualified (clean), qualified (with exceptions), or adverse (significant issues identified), providing users with the auditor’s overall assessment of the control environment.

Management’s Assertion

Contains management’s formal statement regarding:

- Accuracy and completeness of the system description

- Appropriateness of control design

- Operating effectiveness of controls (Type II only)

- Disclosure of any significant changes during the report period

This assertion establishes management’s responsibility for the control environment and provides context for the auditor’s opinion.

Location

Details the physical and logical locations where services are provided, including:

- Data centers and processing facilities

- Administrative offices

- Disaster recovery sites

- Cloud environments

Location information helps users understand the geographic distribution of services and associated risks.

Processes, People, and Systems

Provides comprehensive description of:

- Business processes supporting services

- Organizational structure and responsibilities

- Information systems and technology infrastructure

- Control environment and risk management approach

This section gives users detailed understanding of how services are delivered and controlled.

Subservice Organizations

Identifies third parties that provide critical components of the service, including:

- Nature of services provided

- Controls managed by the subservice organization

- Monitoring performed by the service organization

- Whether the subservice organization is included in the report scope

This information helps users understand dependencies on external parties and associated control considerations.

Complementary User Entity Controls (CUECs)

Specifies controls that users must implement to achieve overall control objectives, such as:

- User access management responsibilities

- Configuration requirements

- Monitoring obligations

- Data input controls

- Output verification procedures

CUECs clarify the division of control responsibilities between the service organization and its users.

Testing Procedures and Results

Details the methods used to evaluate controls and the outcomes of that testing, including:

- Testing methodologies for each control

- Sample sizes and selection criteria

- Test results and observations

- Exceptions identified during testing

- Management responses to exceptions

This section provides transparency into the audit process and the basis for the auditor’s conclusions.

Ensuring Ongoing SOC 1 Compliance

Maintaining SOC 1 compliance between audit cycles requires systematic processes for monitoring and improving controls:

Regular Internal Audits & Readiness Assessment

Implement a continuous assessment program including:

- Quarterly control self-assessments by control owners

- Semi-annual internal audit reviews

- Annual comprehensive readiness assessments

- Ongoing monitoring of control performance metrics

- Regular validation of evidence quality and availability

These activities identify potential issues early and maintain control effectiveness throughout the audit cycle.

Employee Training

Develop comprehensive training programs addressing:

- General SOC 1 awareness for all staff

- Role-specific control responsibilities

- Evidence collection and documentation requirements

- Exception handling and escalation procedures

- Regulatory and compliance updates

Training should be provided during onboarding, after significant changes, and through regular refresher sessions.

Vendor & Third-Party Risk Management

Establish robust oversight of service providers through:

- Comprehensive vendor due diligence

- Contractual security and control requirements

- Regular vendor performance assessment

- Review of vendor compliance certifications

- Monitoring of vendor control changes

- Contingency planning for vendor failures

Effective vendor management ensures that third-party relationships don’t compromise your control environment.

Change Management

Implement structured processes for managing changes to systems and controls:

- Formal change request and approval workflows

- Impact assessment for proposed changes

- Testing requirements before implementation

- Documentation updates reflecting changes

- Communication to affected stakeholders

- Post-implementation verification

Proper change management prevents unintended control degradation and maintains documentation accuracy.

Incident Response

Develop comprehensive procedures for addressing control failures:

- Clear incident identification criteria

- Structured escalation protocols

- Defined roles and responsibilities

- Documentation requirements

- Root cause analysis procedures

- Corrective action processes

- Stakeholder communication templates

Effective incident response minimizes the impact of control failures and demonstrates commitment to maintaining control effectiveness.

Data Protection & Encryption

Implement robust safeguards for sensitive financial information:

- Data classification frameworks

- Encryption for data at rest and in transit

- Access controls based on least privilege

- Data loss prevention technologies

- Secure disposal procedures

- Regular security assessments

These protections ensure that financial data remains secure throughout its lifecycle.

How Network Intelligence Empowers SOC 1 Compliance

Network Intelligence transforms SOC 1 compliance from a resource-intensive manual process into a streamlined, automated program that enhances both efficiency and effectiveness.

Ready to transform your SOC 1 compliance program? Network Intelligence’s compliance experts can provide personalized guidance on implementing automated, efficient compliance processes tailored to your specific organizational needs. Contact us today to schedule a consultation and compliance assessment.Talk to an Expert